Tax tips to know before filing your 2023 income tax

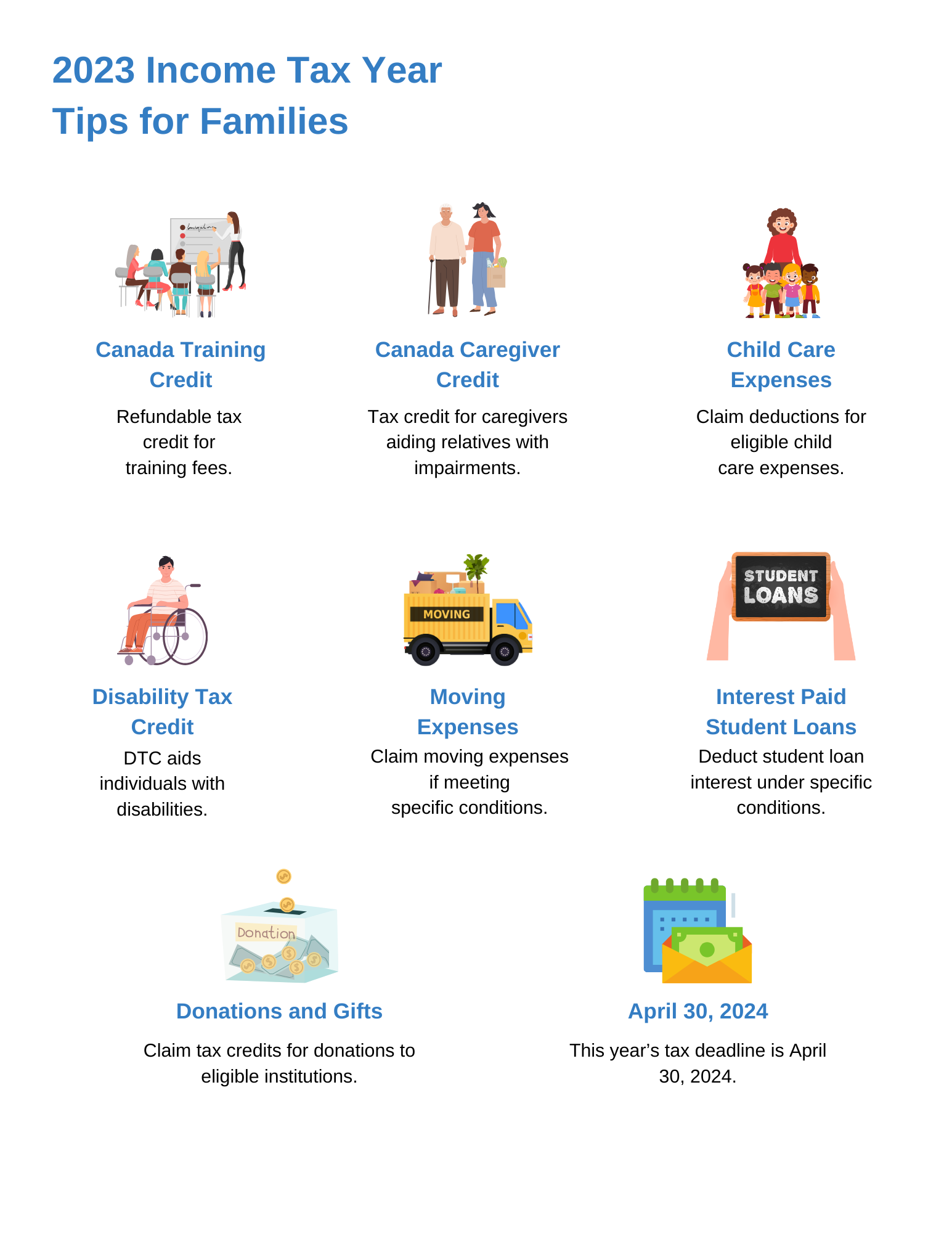

This year’s tax deadline is April 30, 2024. It’s important to make sure you’re claiming all the credits and deductions you’re eligible for. We’ve separated this article into 2 sections:

-

What’s new for 2023

-

Individuals and Families

What’s New for 2023

Advanced Canada Workers Benefit (ACWB)

Automatic advance payments of the Canada Workers Benefit (CWB) are now seamlessly distributed through the ACWB program to individuals who received the benefit in the last tax year. However, it’s important to note that not everyone who received the CWB in the previous tax year will automatically receive the ACWB payments. Only individuals who filed their 2022 tax return before November 1, 2023, are eligible for the ACWB payments.

Furthermore, it’s worth mentioning that the ACWB program eliminates the need to file Form RC201. Recipients are no longer required to fill out this form. Instead, starting in 2023, individuals should report the amounts from their RC210 slip on Schedule 6, Canada Workers Benefit, of their tax return. Additionally, for eligible spouses, the option to claim the basic amount for the CWB is available regardless of who received the RC210 slip.

Deduction for Tools (Tradespersons and Apprentice Mechanics)

Starting in 2023, the maximum employment deduction for eligible tools of tradespersons has risen from $500 to $1,000. Consequently, the threshold for expenses eligible for the apprentice mechanics tools deduction has also been adjusted.

Temporary Flat Rate Method for Home Office Expenses

For the year 2023, the temporary flat rate method for claiming home office expenses is not applicable. Consequently, taxpayers seeking to claim such expenses for 2023 must utilize the detailed method and obtain a completed Form T2200, Declaration of Conditions of Employment, from their employer.

Federal, Provincial, and Territorial COVID-19 repayments

Repayments of COVID-19 benefits at the federal, provincial, and territorial levels, made after December 31, 2022, can be deducted and claimed.

First Home Savings Account (FHSA)

The FHSA is a registered plan designed to aid individuals in saving for their first home. Starting April 1, 2023, contributions made to an FHSA are typically deductible, and eligible withdrawals made from an FHSA for purchasing a qualifying home are tax-free.

Property Flipping

Starting January 1, 2023, any profit generated from the sale of a housing unit (including rental properties) situated in Canada, or a right to acquire a housing unit in Canada, that you owned or held for less than 365 consecutive days prior to its sale is considered business income rather than a capital gain. This is applicable unless the property was already classified as inventory or the sale occurred due to, or in anticipation of specific life events.

Multigenerational Home Renovation Tax Credit (MHRTC)

The MHRTC is a refundable tax credit designed to enable eligible individuals to seek reimbursement for specific renovation expenses incurred in establishing a secondary unit within an eligible dwelling. This enables a qualifying individual to live with their qualifying relative. If eligible, you can claim up to $50,000 in qualifying expenditures for each renovation project completed, with a maximum credit of $7,500 for each eligible claim.

Fuel Charge Proceeds Return to Farmers Tax Credit

The Fuel Charge Proceeds Return to Farmers Tax Credit is now accessible to self-employed farmers and individuals involved in a partnership operating a farming business with one or more permanent establishments located in Alberta, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, Prince Edward Island, or Saskatchewan. If eligible, you may be entitled to a refund of a portion of your fuel charge proceeds.

For Individuals and Families

Canada Training Credit (CTC)

The CTC is a refundable tax credit available to help Canadians with the cost of eligible training fees.

To qualify for the CTC, you need to fill out Schedule 11 for the following:

-

Tuition fees and other applicable fees paid to an eligible educational institution in Canada for courses taken in 2023.

-

Fees paid to specific organizations for occupational, trade, or professional examinations undertaken in 2023.

To be eligible for the CTC, you must meet all these conditions:

-

You resided in Canada for the entire year of 2023.

-

You were at least 26 years old but less than 66 years old at the end of the year.

-

Your most recent notice of assessment or reassessment for 2022 shows a Canada Training Credit Limit for 2023.

Canada Caregiver Credit (CCC)

The CCC is a non-refundable tax credit aimed at assisting individuals who provide support to a spouse, common-law partner, or dependent with a physical or mental impairment, as outlined by the CRA.

You might be eligible for the CCC if you aid:

-

Your spouse or common-law partner dealing with a physical or mental impairment.

-

Dependents such as children, grandchildren, parents, grandparents, siblings, uncles, aunts, nieces, or nephews residing in Canada, who rely on you for consistent provision of basic needs like food, shelter, and clothing.

The amount you can claim varies depending on your relationship to the individual, your circumstances, their net income, and whether other credits are claimed for them.

Child Care Expenses

Child care expenses encompass payments made by you or someone else to arrange care for an eligible child. This care allows you to participate in income-earning activities, pursue education, or conduct research funded by a grant.

If you qualify, you can claim certain childcare expenses as deductions when you file your personal income tax return.

Disability Tax Credit (DTC)

The DTC is a non-refundable tax credit designed to support individuals with disabilities, or their family members who provide support, by reducing their income tax responsibilities.

To be eligible for this credit, individuals must have a significant and enduring impairment. Once approved, they can apply the credit when filing their taxes.

The DTC aims to ease some of the extra costs linked with the disability by lessening the individual’s income tax burden.

Moving

You can claim moving expenses you paid during the year if you meet these conditions

-

You moved to a new residence for work reasons, to start a business in a different area, or to attend a post-secondary program as a full-time student at a university, college, or other educational institution.

-

Your new residence must be at least 40 kilometres closer, determined by the shortest public route, to your new work location or educational institution.

Interest Paid on Student Loans

You might qualify to claim an amount for the interest paid on your student loan for post-secondary education if it was obtained under the following acts:

-

Canada Student Loans Act

-

Canada Student Financial Assistance Act

-

Apprentice Loans Act

-

Provincial or territorial government laws that are similar to the aforementioned acts.

Only you, or a person related to you, can claim the interest paid on the loan within the tax year 2023 or the preceding 5 years.

Donations and Gifts

When you or your spouse/common-law partner donate to eligible institutions, you might be eligible for federal and provincial/territorial non-refundable tax credits when you file your income tax and benefit return.

Normally, you can claim a portion or the full eligible donation amount, capped at 75% of your net income for the tax year.

Seeking guidance?

Wondering if you qualify for valuable tax credits or deductions? Reach out to us – as your financial advisor, we’re here to assist you in optimizing your finances and maximizing your savings.

Canada Training Credit: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-45350-canada-training-credit.html

Canada Caregiver Credit: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/canada-caregiver-amount.html

Disability Tax Credit: https://www.canada.ca/en/revenue-agency/services/tax/individuals/segments/tax-credits-deductions-persons-disabilities/disability-tax-credit.html

Interest Paid on Student Loans: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-31900-interest-paid-on-your-student-loans.html

Donations and Gifts: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-34900-donations-gifts.html

%20in%20Canada.jpg)